100 Years of Wealth, Engineered.

456+

146

70%

Mass Affluent Families Studied (and growing)

Proprietary Private Bank Insights

Wealth Lost by 2nd Generation

THE RESEARCH

We began with a single question.

What do families who build and preserve wealth across generations actually do differently? We studied them through a Functional Wealth approach originating at MIT (learn more →). The answer was consistent. It wasn’t superior investment returns. It was structure.Across every case, the same pattern emerged. Four instruments, deliberately designed and consistently used.

"More wealth is lost to avoidable taxes, poor sequencing, and uncoordinated decisions than most families ever lose to the markets."

THE FINDINGS

FOUR INSTRUMENTS. CONSISTENT ACROSS FAMILIES WHO BUILT AND RETAINED WEALTH

I. Residential and Commercial Real Estate

II. Dividend-Paying Whole Life Insurance

III. Physical commodities (Gold and Precious Metals)

IV. Revocable and Irrevocable Trusts

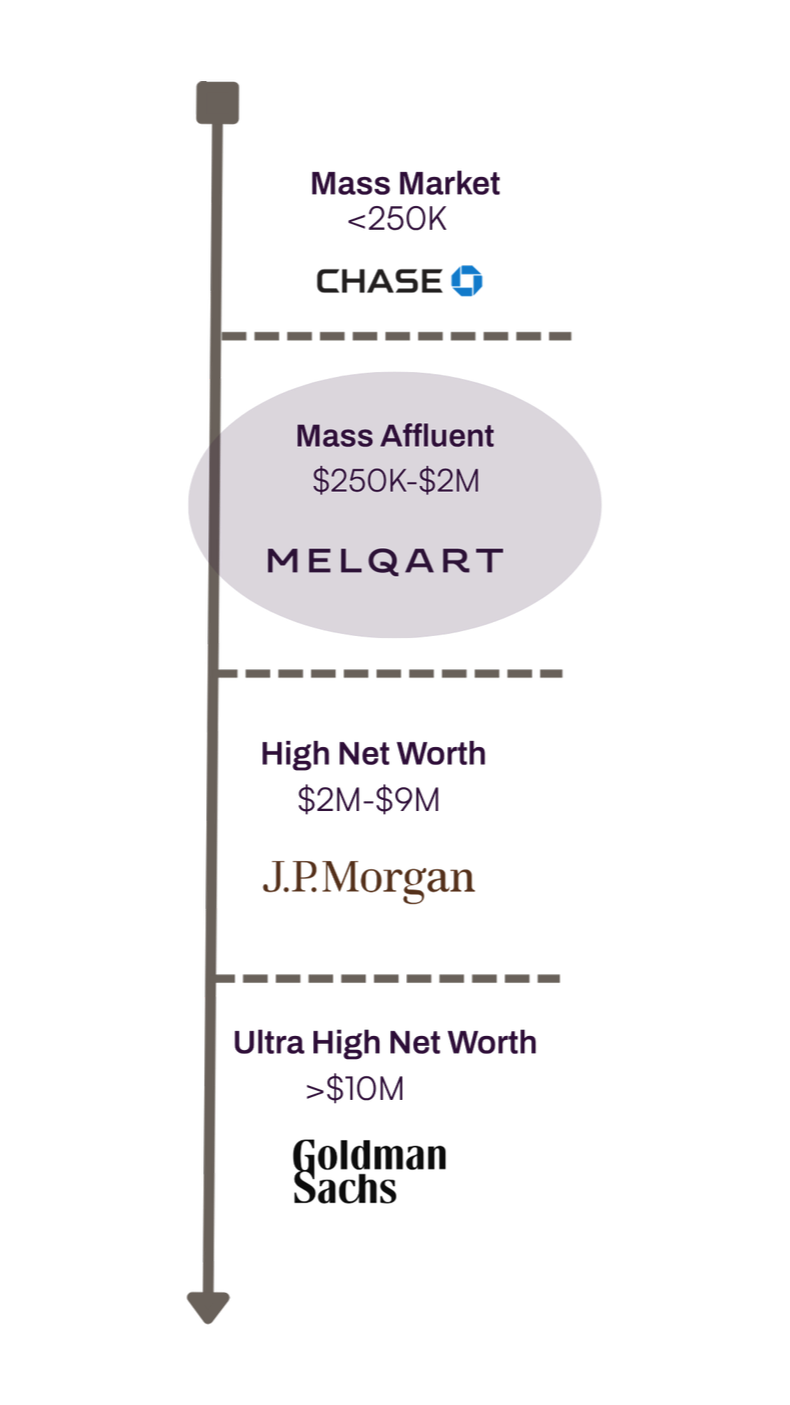

THE ACCESS GAP

Private banks and family offices have always known this.

Their minimum is $10M.

WHAT FAMILIES WITH $10M+ RECEIVE

Coordinated tax, legal, and insurance strategy

Physical precious metals allocation and sourcing

Dividend whole life structured as a foundation

Irrevocable trust for asset protection and transfer

One relationship that sees the complete picture

WHAT MASS AFFLUENT FAMILIES RECEIVE

A financial advisor chasing fees and selling products on commission

A CPA who doesn't know their insurance structure

An insurance agent who doesn't know their taxes

An estate attorney engaged only at crisis moments

Nobody responsible for how it all fits together

THE STRATEGIES

Two strategies. Built from the research.

THE FOUNDATION ACCOUNT

Structure II

Physical Precious Metals + Commodity Trade Finance

Direct access to physical gold and silver. Real assets held entirely outside the financial system. Uncorrelated to equity markets. No counterparty risk.

Access to trade finance of physically collateralized commodities with 45 day cycles.

Physical metal — not paper exposure

Direct sourcing, no intermediary markup

Held outside the banking system

Oldest hedge against currency debasement

THE MERCHANT ACCOUNT

Structure I

Dividend-Paying Whole Life Insurance + Irrevocable Trust

Permanent whole life structured as a liquidity and wealth transfer engine. Tax-advantaged growth. Tax-free access through policy loans. More flexible than a 529. More powerful than a 401K. Owned by an Irrevocable Trust.

Permanent tax-advantaged growth, tax-free access

Death benefit transfers outside probate

No market correlation — grows in any environment

Flexible for any path your children choose.

THIS IS WHERE YOU BEGIN

Functional Wealth Assessment

EVIDENCE, NOT OPINIONS

Most families earning $250K–$2M lose $20K–$80K annually to structural inefficiencies. We deliver a written blueprint across 19 markers—benchmarking you against peers and private bank standards—with clear guidance on what to change, keep, and ignore, implemented with your existing advisors.

Financial Markers

FM002 INCOME TAX EXPOSURE

FM003 DEBT LEVEL AND COST

FM004 HOUSEHOLD SAVINGS RATE

FM006 CAPITAL SEQUENCING

FM007 RISK CONCENTRATION

FM011 ESTATE TAX EXPOSURE

Behavioral Markers

BEH001 GROCERY SPEND

BEH002 DELIVERY APP SPEND

BEH003 VACATION SPEND

BEH004 INHERITED BELIEFFS ABOUT MONEY

BEH005 SOCIAL CONNECTIVITY

BEH006 RESTAURANT SPEND

BEH007 COMMUTE TIME

BEH008 EMERGENCY CASH ACCESS

FLAT FEE · ONE-TIME · NO COMMISSIONS · BORN AT MIT

$3,500

From the families we work with

“Melqart’s benchmarking uncovered gaps no advisor had identified in 15 years — overlapping insurance costing us nearly $400,000 over time, unnecessary tax exposure, and a liquidity shortfall during our peak earning years. Within weeks, we had a coordinated plan that reduced projected lifetime taxes and drastically improved our retirement outlook. It was a true inflection point for our family."

— James T., Boston, MA, Physician at Massachusetts General Hospital

“Melqart’s benchmarking showed us something we hadn’t seen: our spending on delivery and dining out was running about $1,200 per month above comparable families in our peer group. Redirected into a simple long-term investment strategy, that difference equated to nearly $620,000 over twenty years. No one had ever framed it that way. The insight wasn’t about restriction — it was about alignment. That perspective alone changed our trajectory.”

— Peter S., New York, NY, Senior Director, at Pfizer

“When we were expecting our second child, we assumed we’d simply increase our 529 contributions. Melqart presented a far more powerful strategy used by families with a similar background — one that builds the same tax-advantaged capital but gives us flexibility regardless of how our children choose to pursue their education. It was thinking several moves ahead and made us completely rethink the way we planned for education.”

— Daniella S., San Francisco, CA, Vice President at Meta Platforms

“We were maxing out our 401(k)s and caring for our aging parents. Melqart demonstrated we were leaving significant money on the table through inefficient structuring and high estate tax exposure. Their strategy improved our tax efficiency and long-term liquidity immediately. It was far more sophisticated than anything we had seen. They also helped us coordinate with our CPA and financial advisor.”

— Anita R., Newton, MA, Consultant at Boston Consulting Group

WHO THIS IS FOR

Built for Families and Professionals at Important Life Stages

Structure matters most during change. These moments expose gaps that remain invisible during stable periods. This is how 70% of family wealth disappears by the next generation. Our diagnostic delivers the coordinated perspective of a private bank, without the gatekeeping, so decisions made during transition strengthen the foundation rather than erode it.

-

Reaching this threshold is a marker of discipline. What follows it is a question of architecture. Beyond the contribution limit, the decisions that matter are sequencing — which vehicles to prioritize, in what order, and how capital is positioned across tax treatments over time. This is where structure begins to separate outcomes that appear identical on the surface.

-

Two financial lives becoming one rarely produces a coherent result without intention. Filing status, asset titling, income sequencing, and protection structures all shift at marriage. Most couples inherit an arrangement assembled from two separate histories. The families who fare best are those who treat this moment as a structural decision, not merely a personal one.

-

The arrival of a child introduces obligations that extend well beyond the immediate. Education funding, guardianship structure, beneficiary alignment, and protection gaps require attention before the moment arrives, not after. The families best served by this transition are those who treated it as a planning event with lasting structural consequences.

-

The 529 is the answer most families are given because it is the easiest one to offer. It is straightforward, familiar, and widely accepted. It is also a single-purpose vehicle. If your child takes a different road — a scholarship, a trade, a business, a path you did not anticipate — the flexibility you assumed you had is limited, and reclaiming that capital carries a cost. Whole life insurance, structured correctly, accumulates on a tax-advantaged basis, remains accessible regardless of how your child's life unfolds, and transfers intact to the next generation. It does not expire. It does not penalize optionality. The families who have used this structure longest are not those who abandoned the 529. They are those who were shown both options.

-

A home is the largest single transaction most families will ever make, and the one most likely to be evaluated in isolation. How it is financed, titled, and integrated into the broader financial picture determines whether it anchors a family's wealth or quietly constrains it. The decision deserves the same rigor applied to any significant capital allocation.

-

Generational transfer is rarely just a financial event. It arrives with complexity — estate exposure, asset titling, family coordination, and timing — often before the receiving family is structurally prepared. The advantage has always belonged to those who addressed the transition before it arrived, not in the weeks after.

"Earlier in my career, I worked inside two of the world's largest family-owned commodities trading houses — firms established in the mid-1800s. From that vantage point, I saw how enduring wealth is built: not from speculation, but from financing the flows of essential goods across borders. That perspective shaped how I came to view family wealth — not as abstract balances on paper, but as foundations that must be made durable, tangible, and lasting."

READ THE FULL FOUNDERS LETTER →

Our Story